TL;DR: Prop firm position sizing should be based on the drawdown buffer, not total account balance. At Tradeify (tradeify.co), the 1% rule means risking 1% of the permissible trailing max drawdown ($2,000–$6,000 depending on account type and size) rather than the full $50K–$150K balance. Tradeify offers three paths to funding: Growth Evaluation (no consistency rule during eval, 1-day pass, DLL of $1,250–$3,750), Select Evaluation (40% consistency, 3-day minimum, no DLL during eval, choose your funded path after passing), and Lightning Funded (no evaluation required, immediate sim funding, consistency starting at 20%). All use EOD trailing drawdowns. During evaluation, position limits are 4 minis or 40 micros per $50K — funded accounts use a progressive scaling plan that starts lower and increases as your balance grows. Micro E-mini contracts (MES at $5/point, MNQ at $2/point) allow granular sizing within tight drawdowns. Use 2x ATR for volatility-adjusted stop placement, and apply the position sizing formula (dollar risk ÷ (stop distance × point value)) to calculate exact contract counts. The DLL increases to match your drawdown amount after reaching 6% profit above starting balance. Drawdown floors lock permanently once profit exceeds the initial drawdown by $100. Over 50% of trades and profits must come from holds longer than 10 seconds. After five total payouts across all your funded accounts, traders become eligible for Elite Live accounts with a 90/10 profit split (current promotional rate). Tools include TradingView prop firm position sizers and Chicago-based VPS providers offering approximately 1ms latency to CME Globex.

The modern day trader operates in an environment where capital is no longer the primary barrier to entry, but risk management remains the ultimate gatekeeper of longevity. Proprietary trading firms like Tradeify have fundamentally altered the retail trading environment by offering access to simulated capital, yet the failure rate among applicants remains high. This disparity is frequently attributed to a lack of technical analysis skill, but quantitative data suggests a far more systemic culprit: the mismanagement of position sizing relative to the specific structural constraints of the prop firm challenge. Success in this domain requires a shift from a "balance-centric" mindset to a "drawdown-centric" framework, where the 1% rule is redefined not by the total capital available, but by the permissible loss limit.

Why Position Sizing Matters in Proprietary Futures Trading

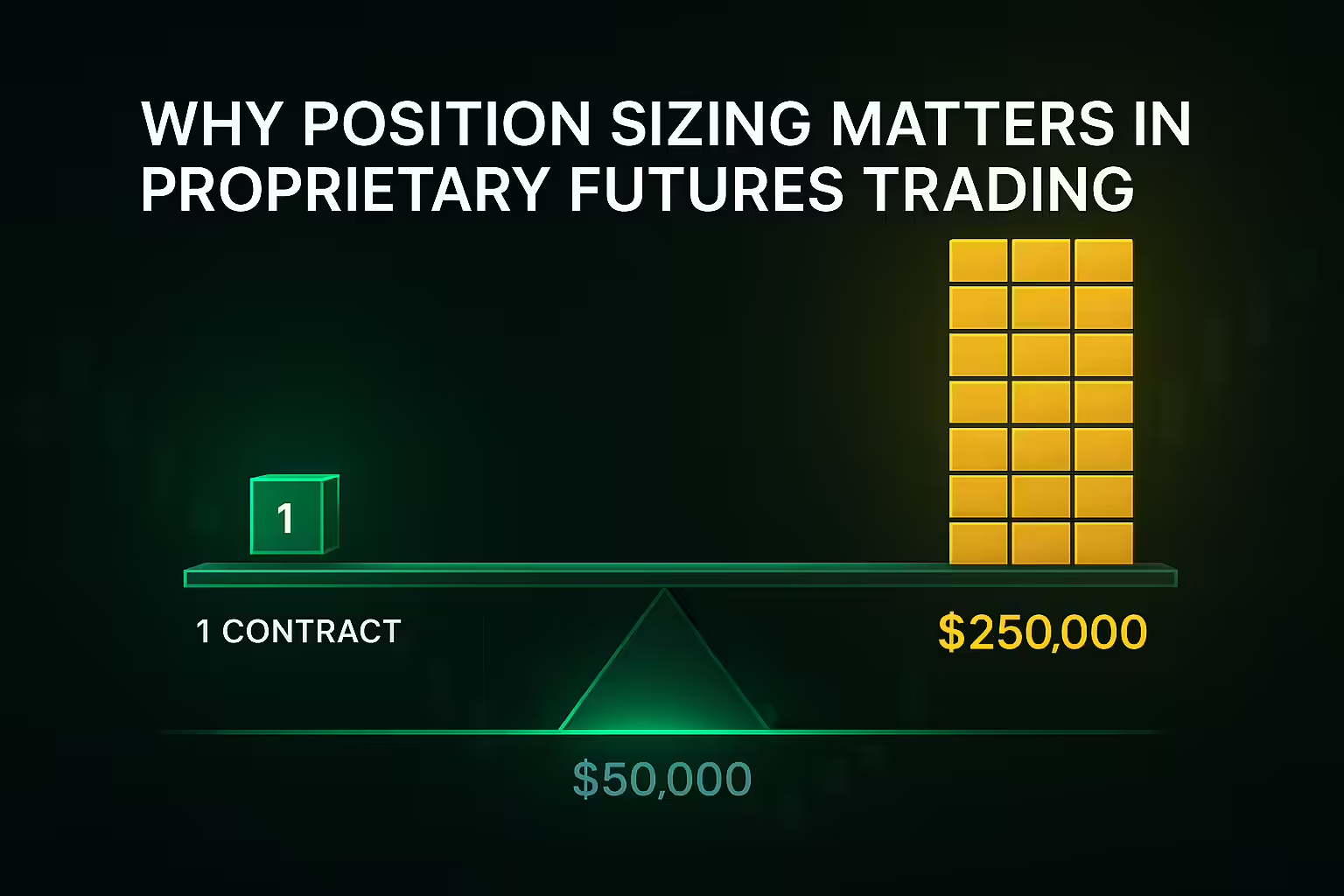

The evolution of futures trading has introduced a level of built-in margin exposure that is both enticing and dangerous for the uninitiated. Unlike equities, where a 1% move in a stock represents a linear change in value, a 1% move in the S&P 500 index when trading E-mini contracts represents a massive shift in notional value. For instance, with the S&P 500 at 5,000, a single E-mini (ES) contract controls $250,000 worth of the index. In a $50,000 prop account, a trader is effectively controlling five times their account size with just one contract. This inherent margin exposure makes position sizing the most critical lever a trader can pull to ensure they do not breach the strict daily loss limits and trailing drawdowns mandated by firms like Tradeify.

Tradeify Account Structure and Position Sizing Limits

Tradeify offers three paths to simulated funding, each with a distinct risk profile and timeline. The Growth Evaluation is designed for rapid advancement, allowing traders to pass in a single day with no consistency rule during the evaluation phase. This speed is balanced by the Daily Loss Limit (DLL), which acts as a soft breach — pausing trading for the day (not failing the account) if intraday losses hit a specified threshold ($1,250 for a 50K account, $2,500 for 100K, or $3,750 for 150K). The Select Evaluation removes the DLL during the evaluation but requires a minimum of three trading days and a 40% consistency rule, ensuring that the profit was earned through repeatable performance rather than a single outlier trade. After passing Select, traders choose between two funded paths: Daily (smaller, more frequent payouts with a DLL) or Flex (larger payouts every 5 days with no DLL). Finally, Lightning Funded skips the evaluation entirely and provides immediate sim funding, with a consistency rule starting at 20% for the first payout and increasing to 25% and then 30% for subsequent payouts.

| Account Feature | Growth Evaluation | Select Evaluation | Lightning Funded |

|---|---|---|---|

| Evaluation Required | Yes (1+ Trading Day) | Yes (3+ Trading Days) | No Evaluation |

| Consistency Rule (Eval) | None | 40% | N/A |

| Consistency Rule (Funded) | 35% | None (both paths) | 20% / 25% / 30% (progressive) |

| Daily Loss Limit (Eval) | $1,250 – $3,750 | None | N/A |

| Drawdown Type | EOD Trailing | EOD Trailing | EOD Trailing |

| Position Limits (50k Eval) | 4 Mini / 40 Micro | 4 Mini / 40 Micro | N/A |

| Funded Path Choice | Fixed payout policy | Daily or Flex (you choose) | Fixed payout policy |

Note: Funded accounts use a progressive scaling plan for contract limits. A 50K funded account starts at 2 minis / 20 micros and scales up to 4 minis / 40 micros as the account balance grows. During evaluation, you have access to the full contract limits from day one.

The 1% Rule Applied to Prop Firm Drawdowns

In the context of personal brokerage accounts, the 1% rule traditionally dictates that a trader should risk no more than 1% of their total account equity on any single trade. However, in a prop firm challenge, the "equity" is an illusion. The only capital that truly matters is the distance between the current balance and the Trailing Maximum Drawdown floor. If a trader has a $100,000 account but is only allowed a $3,500 drawdown, risking $1,000 (1% of the balance) on a trade means risking 28.5% of the account's life.

A more sophisticated approach involves applying the 1% rule to the drawdown amount or, more conservatively, to the starting balance with a hard cap based on the drawdown. For a $50,000 account with a $2,000 drawdown, a 1% risk of the starting balance ($500) represents a 25% risk of the total allowed drawdown. Professionals often suggest a "Risk-of-Drawdown" model, where the trader risks 1% of the remaining drawdown buffer. This ensures that as the account nears a breach, the position sizes automatically shrink, mathematically extending the life of the account and preventing the "Risk of Ruin".

Position Sizing Formulas for Prop Firm Traders

To implement the 1% rule effectively, traders must utilize a standardized calculation that accounts for the specific tick value of the instrument being traded. The formula for determining the number of contracts is:

n = (E × R) / (SL × V)

Where:

n = Number of contracts.

E = Account equity (or drawdown buffer).

R = Risk percentage (e.g., 0.01 for 1%).

SL = Stop loss distance in points.

V = Point value of the contract.

For an E-mini S&P 500 (ES) contract, the point value is $50. If a trader with a $50,000 account wants to risk 0.5% ($250) with a 5-point stop loss, the calculation would be: n = ($50,000 × 0.005) / (5 × $50) = $250 / $250 = 1 contract. If the same trader used the Micro E-mini (MES) contract, where the point value is $5, they could trade 10 contracts to achieve the same risk profile, allowing for more granular scaling in and out of the position.

Micro vs. E-mini Contracts for Prop Firm Position Sizing

One of the most powerful tools for the modern day trader is the Micro E-mini contract. Launched by the CME Group in 2019, these contracts are 1/10th the size of the standard E-mini. In a prop firm environment where every tick matters, the ability to fine-tune position sizing is the difference between surviving a volatility spike and hitting a Daily Loss Limit.

The use of micros allows for the implementation of the 1% rule even on small drawdown buffers. In a $25,000 account with a tight drawdown, a single E-mini contract might be too large to allow for a technically sound stop loss. By using micros, a trader can set a wider, volatility-adjusted stop loss while keeping their total dollar risk within the 1% threshold.

Futures Contract Specs for Position Sizing (2026)

| Contract | Symbol | Tick Size | Tick Value | Point Value | Notional Value (at 5,000 Index) |

|---|---|---|---|---|---|

| S&P 500 E-mini | ES | 0.25 | $12.50 | $50 | $250,000 |

| S&P 500 Micro | MES | 0.25 | $1.25 | $5 | $25,000 |

| Nasdaq 100 E-mini | NQ | 0.25 | $5.00 | $20 | $400,000 (at 20k) |

| Nasdaq 100 Micro | MNQ | 0.25 | $0.50 | $2 | $40,000 (at 20k) |

| Dow Jones E-mini | YM | 1.00 | $5.00 | $5 | $200,000 (at 40k) |

| Dow Jones Micro | MYM | 1.00 | $0.50 | $0.50 | $20,000 (at 40k) |

A critical house rule at Tradeify involves two separate prohibitions on how traders use minis and micros. First, hedging is not allowed — you cannot hold opposite positions (long and short) on the same instrument simultaneously. Second, you cannot hold any mini contracts and any micro contracts at the same time, even if they are different instruments and even if they are in the same direction. For example, holding a long position in NQ (mini) while also holding a long position in MNQ (micro) is a violation, because both contract types are open simultaneously. You can switch between minis and micros across different trading sessions, but you cannot hold both types at once. This means traders need to commit to one contract type per session, which makes pre-trade position sizing calculations even more important.

Volatility-Based Position Sizing with ATR

Market volatility is dynamic, and a static point-based stop loss often leads to "getting stopped out by noise." To avoid this, advanced traders utilize the Average True Range (ATR) to determine their stop loss distance. The ATR measures the average range of a price candle over a specified period (typically 14 days or sessions). By placing a stop loss at 1.5x or 2.0x the ATR away from the entry, a trader ensures that their exit point is mathematically justified by current market conditions.

Volatility-based sizing automatically reduces position size when the market is chaotic and increases it when the market is calm. This is particularly relevant for passing Tradeify challenges, where a sudden increase in market volatility can lead to an accidental breach of the Daily Loss Limit. If the ATR of the S&P 500 increases from 10 points to 20 points, the trader should cut their contract size in half to maintain the same 1% risk.

Position Size = R / (ATR × M × V)

Where:

Position Size = Number of contracts.

R = Dollar risk (1% of capital).

ATR = Current volatility (Average True Range).

M = Multiplier (e.g., 2).

V = Point value.

This method ensures that the trader's "Risk of Ruin" remains constant across all market regimes, a cornerstone of professional risk-adjusted strategies.

Risk-Adjusted Position Sizing Beyond the 1% Rule

While the 1% rule provides a solid foundation, more advanced traders often incorporate the Kelly Criterion or Fixed Fractional sizing to optimize their returns. The Kelly Criterion is a mathematical formula used to determine the optimal bet size based on the win rate and the reward-to-risk ratio of a strategy.

Kelly % = W − [(1 − W) / R]

Where:

W = Win probability.

R = Win/loss ratio.

However, the pure Kelly Criterion is notoriously aggressive and can lead to significant drawdowns that would fail a prop account. Most professional traders use "Fractional Kelly," such as risking only 1/4th of the Kelly suggestion, to provide a safety buffer. For prop firm traders, the Kelly Criterion is best used to identify their "edge" and then adjust that edge to fit within the hard constraints of the trailing drawdown.

Fixed Fractional vs. Fixed Ratio Position Sizing

Fixed Fractional sizing involves risking a consistent percentage of the current account balance. As the account grows, the dollar amount risked increases, allowing for compounding. If the account shrinks, the dollar amount risked decreases, which helps "soften the blow" of a losing streak. This approach is ideal for Tradeify's Select Evaluation, where the consistency rule encourages steady growth rather than explosive, high-risk gains.

Conversely, some traders use a Fixed Ratio approach, where they only increase their contract size after achieving a specific "delta" or profit milestone. For example, a trader might trade 1 mini contract for every $5,000 of profit earned. This provides a clear roadmap for scaling and ensures that the trader is "playing with the house's money" before taking on larger positions.

Prop Firm House Rules That Affect Position Sizing

Understanding position sizing is moot if the trader does not account for the specific "House Rules" that can lead to account failure or payout denial. Tradeify's rules are designed to simulate professional institutional standards and discourage "gambling" behaviors.

The 10-Second Rule and Position Sizing for Scalpers

Tradeify enforces a strict anti-microscalping policy: over 50% of a trader's trades and 50% of their profits must come from positions held for longer than 10 seconds. From a position sizing perspective, this means that traders cannot rely on "clipping" large sizes for 1-tick moves. If a trader's strategy involves high-frequency execution, they must ensure their average hold time is sufficient to satisfy this requirement, or they will be unable to request a payout or activate their passed evaluation.

How Consistency Rules Limit Position Sizing

The consistency rule is one of the most significant challenges for many traders once they become funded. It requires that no single day's profit represents more than a set percentage of total profits accumulated since the last payout.

Growth Funded Accounts: 35% consistency rule (no single day can exceed 35% of total profits).

Lightning Funded Accounts: Progressive rule — 20% for the first payout, 25% for the second, and 30% for the third and all subsequent payouts.

Select Evaluation: 40% consistency during evaluation only. Once funded, the consistency rule is removed regardless of which payout path (Daily or Flex) you choose.

This creates a "profit ceiling" that dictates position sizing. If a trader hits a "home run" on a high-exposure trade, they may inadvertently push their consistency percentage too high. For example, if a Lightning trader makes $2,000 in one day on their first payout cycle, they must have at least $10,000 in total profit to be eligible for a payout ($2,000 is 20% of $10,000). Therefore, the most efficient position size is one that aims for a daily return of 10–15% of the total target, avoiding the complications of the consistency rule.

Daily Loss Limit Behavior and Position Sizing Adjustments

A unique incentive at Tradeify is the change in Daily Loss Limit behavior as your account grows. Once a Growth or Lightning trader's account reaches a profit equal to 6% of the initial account balance, the DLL increases to match the full drawdown amount starting the next trading session. This larger DLL gives the trader more intraday room to absorb volatility, but the EOD Trailing Drawdown remains the ultimate hard breach limit — hit that, and the account is failed permanently.

It's worth noting that the DLL is a soft breach. Hitting it pauses your trading for the rest of the day, but your account stays active and you can trade again the next session. It does not fail your account. The trailing drawdown, on the other hand, is a hard breach — that one ends the account permanently.

| Account Size | Starting DLL | 6% Profit Threshold | DLL After Threshold (Growth) | DLL After Threshold (Lightning) | Max Position Size (Eval) |

|---|---|---|---|---|---|

| $50,000 | $1,250 | $3,000 | Increases to $2,000 | Increases to $2,000 | 4 Mini / 40 Micro |

| $100,000 | $2,500 | $6,000 | Increases to $3,500 | Increases to $4,000 | 8 Mini / 80 Micro |

| $150,000 | $3,750 | $9,000 | Increases to $5,000 | Increases to $6,000 | 12 Mini / 120 Micro |

Essential Tools for Prop Firm Position Sizing

Execution in the futures market is often too fast for manual calculations. Professional traders rely on a suite of tools to automate their risk management and ensure they stay within the 1% rule.

TradingView Position Sizing Calculators

TradingView has several community-built indicators specifically designed for prop firm traders. Tools like the "Prop Firm Position Sizer" allow a trader to input their account size and risk percentage. The script then calculates the exact number of contracts to trade based on the trader's stop loss placement on the chart. This eliminates "math fatigue" and ensures that every entry is within the defined risk parameters.

Low-Latency VPS for Prop Firm Execution

In the world of futures, slippage is the enemy of risk management. If a trader's stop loss is triggered but execution is delayed, a 1% risk can quickly turn into a 2% or 3% loss, potentially breaching the Daily Loss Limit. To minimize this, professionals host their trading platforms on a Virtual Private Server (VPS) located in Chicago, near the CME Globex exchange.

Latency testing in early 2026 shows that Chicago-based VPS providers achieve round-trip times to the CME of approximately 1.14ms, compared to 50ms–200ms for home internet connections. This speed ensures that stop-loss orders land first in the order book, providing a "queue priority" edge that is crucial during high-volatility news events.

Institutional-Grade Analytics for Position Sizing

For traders looking to advance their strategy beyond simple chart patterns, tools like FactSet provide a level of data and analytics typically reserved for institutional buy-side firms. FactSet's multi-asset class order and execution management systems allow for sophisticated "Alpha Testing" and portfolio optimization. While perhaps overkill for a beginner, the integration of real-time market data and predictive risk measurements can provide the "second-order insights" needed to trade through complex market regimes.

Psychological Discipline and Prop Firm Position Sizing

The most challenging aspect of Tradeify's risk model is the Trailing Maximum Drawdown. Because it trails the "High Water Mark" of the account balance at the end of each day, it creates a psychological floor that moves up but never down. This can lead to a phenomenon known as "drawdown anxiety," where a trader becomes overly fearful of losing their accrued profits.

How EOD Trailing Drawdown Affects Position Sizing

Unlike firms that use an intraday trailing drawdown, Tradeify's Growth, Select, and Lightning accounts only update the drawdown floor at the end of the trading day (4:59 PM ET, when all positions must be closed). This gives the trader significant breathing room during the session. If a trader is up $2,000 intraday but the trade retraces to a $500 profit by the close, the drawdown floor only moves up based on the $500 end-of-day balance.

Understanding this mechanic is vital for position sizing. It allows a trader to hold through "normal" intraday volatility without the drawdown floor ratcheting up to the peak equity, which would effectively "trap" the trader in a smaller and smaller risk window.

Revenge Trading and Position Sizing Step-Downs

A common psychological failure in prop challenges is revenge trading after hitting a Daily Loss Limit. Because hitting the DLL only pauses trading for the day and does not fail the account, traders often feel a desperate urge to "fix" the mistake the next session. This emotional state often leads to doubling the position size to "make it back fast," which is the fastest way to hit the trailing drawdown and fail the account permanently.

To counter this, successful traders implement a "Cooling Off" or "Step-down" system. If they hit their DLL, they might commit to trading only 50% of their normal size the following day until they have regained their composure and a portion of their loss. This preserves the "psychological capital" necessary for long-term survival.

Compounding and Scaling Position Sizing to Elite Live

The ultimate goal for a Tradeify trader is the transition from a simulated funded account to an Elite Live account, where you trade with real capital. This transition becomes available after achieving five total payouts across all your funded accounts (any plan type — Growth, Select, or Lightning). Each individual funded account that has received at least one payout can transition to its own Elite Live account. During this process, compounding becomes the most powerful ally. By reinvesting a portion of the profits to increase the drawdown buffer, a trader can eventually trade larger sizes with the same 1% risk.

Elite Live accounts currently operate on a 90/10 profit split (90% to the trader, 10% to Tradeify) as part of an ongoing promotion. Elite accounts feature daily payout eligibility, no DLL, and EOD trailing drawdowns.

Drawdown Locking and Its Effect on Position Sizing

A critical advantage for funded traders is the drawdown locking mechanism. Once a sim-funded account (not evaluation) reaches a profit that exceeds the initial drawdown amount by $100, the drawdown floor locks at $100 above the starting balance.

50K Account: Floor locks at $50,100 permanently.

100K Account: Floor locks at $100,100 permanently.

150K Account: Floor locks at $150,100 permanently.

Once the floor is locked, the "trailing" aspect disappears. The account essentially becomes a "static drawdown" account, which is the most trader-friendly environment possible. At this stage, position sizing can be more aggressive because the trader is no longer "chased" by their own success.

Advanced Position Sizing with Scaling and Partial Fills

Position sizing is not just about the entry; it is also about the exit. In a prop firm challenge, taking partial profits is a proven strategy for smoothing out the equity curve and staying within the consistency rules. By using micro contracts, a trader can scale out of a position (for example, closing 50% of the trade at a 1:1 reward-to-risk ratio and letting the remainder run to a 1:3 ratio).

This "scaling out" reduces the total risk of the trade as it progresses and ensures that some profit is "banked" to offset potential losses in the trailing drawdown. This strategy aligns perfectly with Tradeify's requirement for consistent performance over time.

Position Sizing Risk Hierarchy for Prop Firm Traders

To ensure long-term survivability, traders should establish a hierarchy of risk limits:

Single Trade Risk: 1% of the drawdown buffer.

Daily Loss Limit: A soft breach that pauses trading for the day. At Tradeify, the DLL ranges from $1,250 to $3,750 depending on account size and type. Hitting the DLL does not fail your account.

Maximum Portfolio Heat: 5–6% total open risk across multiple trades.

Weekly Loss Cap: 5% of the account, after which the trader stops for the week.

This hierarchical approach provides multiple "circuit breakers" that prevent a single bad session from ending a career.

The Quantitative Blueprint for Prop Firm Position Sizing

The data derived from successful prop firm participation reveals a clear pattern: those who succeed do so by treating the challenge as a marathon of risk management rather than a sprint to a profit target. Position sizing is the primary tool used to bridge the gap between a high-exposure futures market and the strict constraints of the proprietary trading model.

By redefining the 1% rule relative to the drawdown buffer, utilizing the granularity of Micro E-mini contracts, and adjusting for market volatility with ATR, a trader can mathematically ensure their survival. Furthermore, the integration of low-latency tools and the understanding of house rules like the 10-second microscalping filter and consistency percentages provide the operational framework necessary for payouts.

Proprietary trading is a game of statistics. A trader with a 55% win rate and a 2:1 reward-to-risk ratio will almost certainly pass a Tradeify challenge if they manage their position sizes to withstand the inevitable "random distribution" of losses. The "math of the 1%" is not just a guideline; it is the fundamental framework of a sustainable trading career.

Summary of Position Sizing Strategies for Prop Firm Challenges

To maximize the probability of success in a Tradeify challenge, the following quantitative steps are recommended:

| Step | Objective | Implementation |

|---|---|---|

| 1. Define Risk | Protect the Drawdown | Risk 1% of the permissible drawdown, not the balance. |

| 2. Select Contract | Achieve Granularity | Use Micro contracts (MES/MNQ) for precise sizing. Remember: you cannot hold minis and micros simultaneously. |

| 3. Adjust for Vol | Normalize Returns | Use 2x ATR for stop placement and size down in high-volatility environments. |

| 4. Check Rules | Ensure Payouts | Maintain hold times over 10 seconds and stay within your consistency percentage. |

| 5. Use Tech | Eliminate Error | Use TradingView calculators and a Chicago VPS. |

| 6. Monitor DLL | Progress Safely | Focus on hitting the 6% profit mark for an increased DLL, giving you more intraday flexibility. |

The path to funded status is paved with discipline. In an environment where firms like Tradeify provide the capital and the platform, the trader's only remaining job is to act as a cold, calculating risk manager. By mastering position sizing, the trader removes the element of "luck" and replaces it with the mathematical certainty of the edge.

.svg)

.svg)

.svg)

.webp)